Opinion,

Value Enhancement – Where Reporting Ends, the Valuation Lever Begins

By Vincent Giesue Furnari, managing partner at Kirchhoff Consult GmbH in Bond Guide magazine.

A Thursday in March. The mid-cap sale process is entering the final stretch; the information memorandum has long since been circulated. One of the lead bidder’s decisive questions is not about pricing. It is about specific climate risks. This is not a challenge to EBITDA, but to the multiple — and therefore to enterprise value. Since the Omnibus package, this has been happening more often, not less.

The EU has eased reporting obligations for around 85% of companies — and at the same time, pressure in the M&A market to disclose robust, defensible ESG profiles is increasing. Anyone who sees a contradiction here is confusing reporting obligations with financial and strategic relevance. For small- and mid-cap sellers, this is precisely where the valuation lever begins.

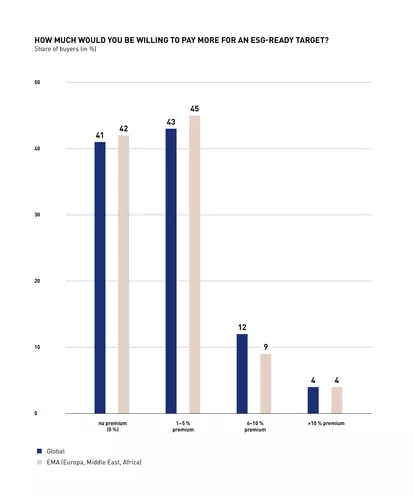

The empirical evidence from 2024/25 dispels the notion that ESG is primarily a reporting issue. According to KPMG’s ESG Due Diligence Study 2024 (n = 743), 55% of buyers are willing to pay a premium of 1% to 10% for an ESG-mature target; a further 4% would pay more than 10%. Only 41% draw the line at zero.

On the other side, Deloitte’s M&A ESG Survey 2024 reports that 72% of surveyed companies have abandoned acquisitions due to ESG red flags — up from 49% in 2022.

What matters is which ESG dimension is actually value-relevant. A study by Ezenwa and Grigorieva (SN Business & Economics, 2025) isolates the strongest driver within ESG dimensions: based on 413 global M&A deals, governance quality has a significantly positive effect on the bid premium, whereas the aggregate ESG score is positive but not statistically significant. This suggests buyers respond less to compressed ESG ratings than to demonstrable governance quality.

For sellers, this means: it is not the aggregate score that matters, but operational substance — documented, traceable, and defensible within the process. The priority is clear: robust governance structures, measurable human-capital and safety metrics, and documented supply-chain compliance. At the negotiating table, it is not the narrative alone that carries weight, but its substantiation through data, evidence, and proven steering capability.

The Small- and Mid-Cap Gap

The Omnibus I reform eases the burden precisely in the segment where most M&A transactions take place: small and mid-caps. Going forward, these companies will largely fall outside mandatory sustainability reporting. However, to deprioritise ESG on that basis would be commercially short-sighted.

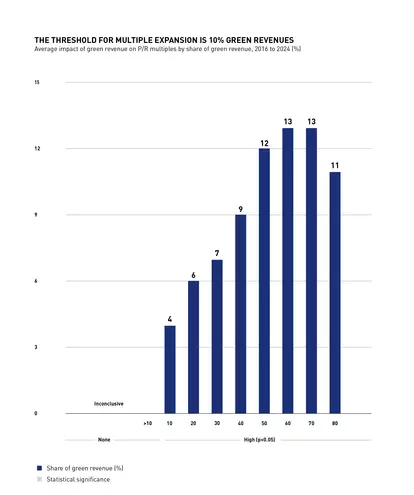

For buyers, ESG remains relevant — first, as a transparency and risk issue, and second, as an indicator of the future viability of the business model. According to Boston Consulting Group (BCG, Green Growth 2025), valuation premia increase with a rising share of climate-related revenues — from around 4% once green revenues reach 10%, up to 13% at a 60% revenue share.

EY-Parthenon and EBS University (November 2024) quantify the effect for private equity funds: portfolios with an AAA ESG profile (RepRisk rating) achieved an IRR of 25.4% in the sample — 7.8 percentage points above BBB funds, and up to eight percentage points higher than ESG-weak competitors overall.

Sell-Side ESG Readiness: A Blueprint, Not a Reporting Exercise

This resolves the apparent contradiction: reporting is becoming easier; valuation is becoming tougher.

The VSME standard provides mid-sized companies with a practical data framework which — taking into account a complete carbon footprint (Scopes 1–3) and a few additional data points — delivers the metrics buyers and lenders now require, without the CSRD overhead.

The methodological mistake in most mid-cap sale processes is bringing ESG in late — and, if at all, treating it as a separate workstream. The typical scenario is this: vendor due diligence is underway, the information memorandum is final, and only then do the first investor questions arrive on emissions baselines, supply-chain due diligence obligations, or diversity metrics — and the sell-side responds defensively. The negotiating position shifts; price haircuts or additional escrow requirements follow.

The effective logic is the reverse: ESG analysis before the process starts, structured in three stages.

- A sober baseline assessment based on double materiality, focused on the levers most likely to translate into revenue, cost structure, or risk premia.

- Implementation of defined work packages with financial quantification, measured against the expected EBITDA impact.

- A report that prepares the outcomes of the value-enhancement process as a robust, data-based foundation for the valuation discussion — not as a marketing brochure.

How far this can go is illustrated by a case documented in the literature from the portfolio of an institutional private equity investor (Greenfield, Monk, Rook – Stanford Long-Term Investing Initiative, January 2026). The portfolio company introduced a differentiated incentive scheme for operational employees, linked to performance and safety metrics.

As a result, the staff turnover rate halved relative to the industry level, avoiding recruitment and training costs in the millions. An improved accident rate reduced insurance premiums by around 37% per unit. Governance protocols to reinforce process discipline further reduced resource consumption and emissions. On the revenue side, the stronger ESG profile expanded access to tenders from customers with their own decarbonisation targets.

In summary, this delivered an EBITDA effect of around USD 16 million and — at a sector-standard multiple of 9x — an enterprise value uplift of roughly USD 144 million, driven solely by ESG mechanics.

This approach is transferable and scalable. Applied to a typical European mid-cap with EUR 50 million EBITDA and a sector-standard multiple of 8x: an identified ESG EBITDA effect of EUR 1 million implies EUR 8 million of additional enterprise value — and at EUR 2 million ESG EBITDA, EUR 16 million. The decisive factor is less the absolute number than the underlying logic: every ESG lever is treated as a line item in P&L mechanics, not as a chapter in a report. The EBITDA bridge reflects the debate with the buyer; the valuation multiple makes the magnitude visible.

Bridge to the Debt Capital Markets

For issuers of SME bonds and for sustainability-linked debt structures, the same mechanics apply in the opposite direction.

Transition finance recommendations from the European Commission (2023, updated 2026) and ICMA’s Climate Transition Finance Handbook guidance call for entity-level transition plans with operational KPIs. Companies that prepare these data for a potential M&A process in any case simultaneously secure access to transition-related financing instruments and, typically, better terms.

Sell-side ESG readiness therefore becomes a dual instrument: an equity valuation lever and a spread argument in one.

Conclusion

If the lead bidder starts challenging the multiple in the final stretch, it is too late. In mid-cap M&A, sell-side ESG readiness is not an appendix topic — it is a valuation argument in its own right, and it only works if it is quantified, documented, and defensible on the negotiating table before the process begins.

Those who achieve this do not merely defend their multiple. They also expand their investor universe — in both the equity and bond markets.

About the Author

Vincent Giesue Furnari is Co-CEO of Kirchhoff Consult GmbH in Hamburg and is responsible for developing advisory products at the intersection of ESG, capital markets, and M&A. His focus is on integrating sustainability value drivers into transaction processes for small and mid-cap companies.

ABOUT KIRCHHOFF CONSULT

With around 70 employees, Kirchhoff Consult is a leading communications and strategy consultancy for financial communications and ESG in German-speaking countries. For more than 30 years, Kirchhoff has been advising clients on all aspects of financial and corporate communications, annual and sustainability reports, IPOs, investor relations and ESG and sustainability communications. 'Designing Sustainable Value': Kirchhoff combines content expertise with excellent design to create sustainable value.

Kirchhoff Consult is a member of TEAM FARNER, a European alliance of partner-led agencies. The common goal: to build the European market leader for integrated communications consulting.

Learn more on: kirchhoff.de

Say Hello.

Vincent Furnari

Managing Partner

vincent.furnari@kirchhoff.de

+49 40 609 186 58